Vietnam's First Billion-Dollar IPO of 2026: Điện Máy Xanh Spins Off, and Every Dong Raised Goes Back to Pay Parent's Debt

MWG is spinning off Vietnam's biggest consumer electronics chain, Điện Máy Xanh, at a near-USD 4 billion valuation — but all proceeds repay the parent's short-term debt, and retail investors get a free float of under 15%.

[Vietnam's First Billion-Dollar IPO of 2026: Điện Máy Xanh Spins Off, and Every Dong Raised Goes Back to Pay Parent's Debt]

On May 22, Vietnam's State Securities Commission (UBCKNN, the country's equivalent of the SEC) issued an IPO certificate clearing the way for Điện Máy Xanh — the consumer electronics chain run by retail group MWG (Mobile World), one of Vietnam's largest brick-and-mortar retailers — to list on the Ho Chi Minh Stock Exchange (HOSE) in early August.

The offering price is set at VND 80,000 per share, putting expected market capitalization near USD 3.9 billion. That makes DMX the first IPO in Vietnam this year to clear the billion-dollar mark. Subscriptions open May 27 and close June 17, with allocations announced June 18-19.

[Who is DMX]

DMX sells televisions, fridges, washing machines and air conditioners. Its green-and-white storefronts are a familiar sight in Vietnam's second- and third-tier cities. The chain sits inside MWG alongside two other major brands — mobile phone retailer Thế Giới Di Động and grocery chain Bách Hoá Xanh — plus the much smaller An Khang pharmacy chain.

By the end of 2025, the group's phone and electronics stores together totaled roughly 3,000 outlets. DMX alone accounted for more than 2,000 of them, making it the largest brand in the group and the main reason MWG posted record consolidated revenue in 2025.

But the past three years tell a different story than aggressive expansion. MWG closed more than 400 underperforming stores and trimmed headcount. Net margins moved up, and inventory turned over faster. DMX is going public as a leaner business, not a growth story chasing new openings.

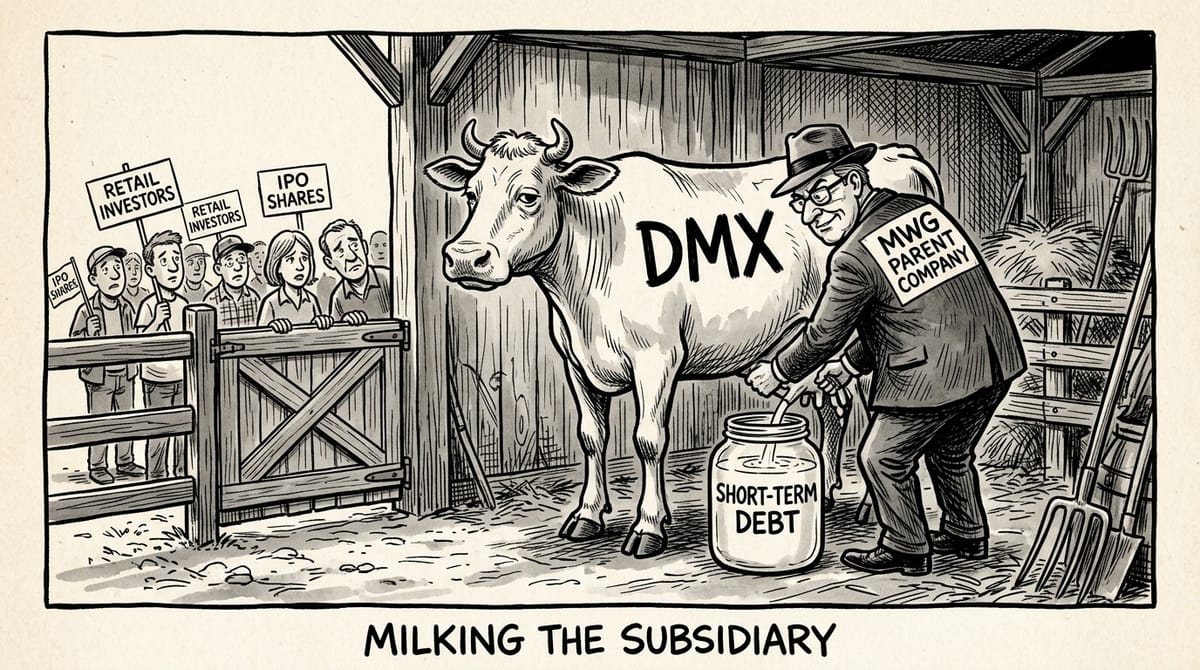

[None of the Proceeds Stay with DMX]

The most telling line in the IPO filing is the use-of-proceeds disclosure. DMX expects to raise about VND 14.36 trillion (USD 546 million). Every dong of it goes to repay short-term loans owed by parent company MWG. Nothing for new stores. Nothing for technology. Nothing held back for new ventures.

The reason becomes clear from MWG's balance sheet. As of the first quarter of 2026, the group carried roughly VND 28 trillion in short-term debt against just VND 4.5 trillion in cash — enough to cover only about 16% of what is coming due. Long-term debt is essentially zero. In other words, MWG's working capital depends on rolling over short-term loans, and the DMX listing is effectively a way to use a subsidiary's valuation to ease pressure on the parent's balance sheet.

[Retail Float Under 15%, Foreign Investors Start from Zero]

The second structural signal is that MWG has no intention of giving up control.

Before the IPO, MWG owns about 99% of DMX. After the listing, it will still hold 85%. The public float sits at just 11% to 14% — low even by the standards of Vietnam's VN30 blue chips, which suggests secondary-market liquidity may disappoint.

For foreign investors, though, the same equation looks different. DMX's foreign ownership cap is set at 49%, and current foreign ownership is zero. Institutions do not need to buy from existing holders — they can build positions directly at the IPO. With FTSE having upgraded Vietnam to secondary emerging-market status, DMX is the rare Vietnamese retail leader where overseas funds can start from a clean slate.

[The "Cash Cow" Framing]

MWG chief executive Vũ Đăng Linh has described DMX as a "cash cow" in interviews. The message is direct: deliver steady dividends, do not chase fast growth. The matching dividend policy is a 40% cash payout for 2026 — VND 4,000 per share, or about 5% yield at the IPO price.

Tie that framing back to the IPO structure and the logic snaps into place. Proceeds flow back to the parent to cut debt, leaving DMX with a lighter balance sheet that supports stable long-term payouts. MWG keeps 85%, so most of the dividends still come back to the parent. And foreign buyers are being sold a long-term income story with exposure to Vietnamese retail — not a short-term price play.

The main beneficiaries here are the parent company and institutional investors. Retail investors are not the core audience.

[CLV: From Selling Appliances to Selling Services]

The story of DMX's upgrade is not only about stores and inventory. The IPO filing dedicates significant space to how the company is turning one-off appliance sales into long-term service relationships. MWG calls this internal playbook "CLV" — customer lifetime value.

Three pieces are in motion:

- The after-sales repair operation has been carved out into a separate subsidiary called Thợ Điện Máy Xanh ("DMX Technicians"), with more than 8,000 technicians nationwide. What used to be an internal maintenance department now operates as a business that can take outside orders, meaning DMX customers no longer touch the brand only once.

- The group's "Quà tặng VIP" super app, the MWG loyalty platform, has been used more than 40 million times, with average in-app order values up nearly 30% year on year. It channels one-off purchases toward extended warranties, accessories and value-added services.

- Prepaid service revenue — extended warranties, scheduled maintenance and similar products — has exploded over the past year, jumping from about VND 2.2 billion at the end of 2024 to more than VND 60 billion in the first quarter of 2026. Customers prepaying DMX is effectively a commitment to keep using the brand for years.

None of this shows up immediately in valuation multiples like P/E. But it will decide whether DMX stays a pure retailer or grows into a service company over the next few years. MWG has already run a version of this playbook in Indonesia through its EraBlue joint venture, which turned profitable in 2025, broke past 180 stores and grew revenue by more than 70% year on year. The model travels — which is why DMX's valuation is not just about selling TVs.

The Viet Media Monthly

A curated monthly digest of the most important political, economic, tech, and industry developments in Vietnam.

Designed for reading on desktop or tablet — no algorithm, no noise. Just the stories that matter.

Delivered before the 10th of each month. Cancel anytime.