Vietnam Stocks Crash Over 100 Points in One Day as Middle East Oil Crisis Hammers Asia

The VN-Index lost over 100 points on March 9 — the biggest single-day drop in Vietnamese stock market history. Oil at USD 118 and margin calls turned a bad week into a historic crash.

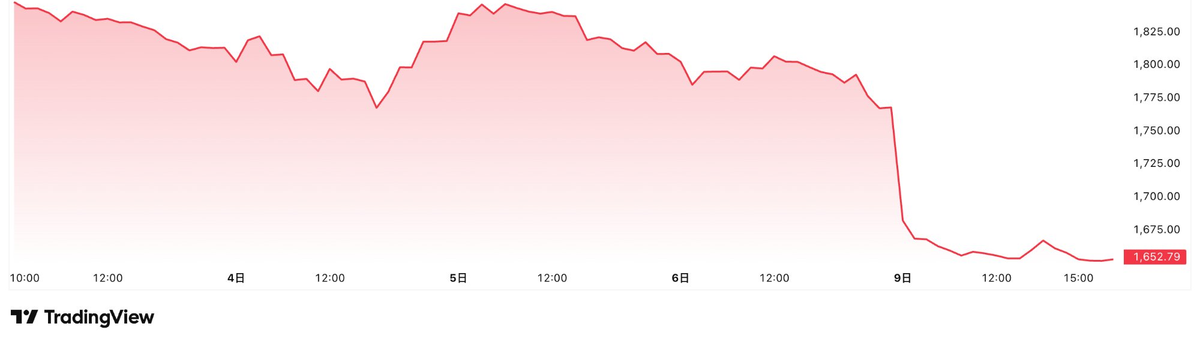

It took 15 minutes.

That's how long it took for the VN-Index to fall more than 100 points on the morning of March 9. The index bottomed at 1,663 and closed near 1,653 — down more than 6% in a single session.

No trading day in Vietnamese stock market history had ever produced a 100-point drop. This one did it before most people had finished their morning coffee.

And March 9 wasn't the beginning. The index had already lost about 112 points over the previous week, sliding from near 1,880 to 1,768. Add Monday's crash, and the VN-Index shed more than 220 points in six trading days.

The Trigger

The catalyst was a sharp escalation in the Middle East.

Military conflict between the US, Israel, and Iran widened in early March. Iran's Revolutionary Guard briefly announced the closure of the Strait of Hormuz. Tehran walked it back on March 6, denying a "complete blockade" — but by then, hundreds of ships were stuck in transit and several major maritime insurers had pulled war risk coverage from the area starting March 5.

Roughly a quarter of the world's oil and a fifth of its liquefied natural gas passes through the Strait of Hormuz. When it's disrupted, energy markets don't wait.

Brent crude hit USD 118 per barrel on March 9. That was a 30% jump in one week.

All of Asia Was Falling

Vietnam wasn't alone. The entire region was in the red.

South Korea's KOSPI crashed over 8%, triggering a circuit breaker that halted trading for 20 minutes — the second activation in four trading days. Samsung Electronics fell more than 13% for the week. SK Hynix dropped nearly as much.

Japan's Nikkei 225 plunged over 7% intraday, closing down about 5.5% and breaking below 53,000.

Vietnam's drop wasn't the deepest in Asia that day. But Vietnam has no market-wide circuit breaker — individual stocks have a 7% daily limit, but nothing pauses the whole market. So the panic ran straight into the prices with no interruption.

Nearly Every Sector Down

Of 21 sectors tracked, 18 fell.

Banking stocks hit the daily floor across the board: ACB, BID, CTG, HDB, SHB, TCB, VPB, TPB — all locked at their lower limits. Every stock in the Vingroup family — VIC, VHM, VRE, VPL — also hit the floor. Tech dropped nearly 12%. Retail fell over 10%. Real estate was down close to 9.5%.

The exceptions were obvious: oil and gas stocks rose over 8%, and fertilizer stocks climbed more than 11%. DPM, DCM, and LAS gained 4% to 5%.

Why It Got So Ugly So Fast

Geopolitical fear set the sell-off in motion. Margin calls made it violent.

When prices drop fast, brokerages and private lending firms demand that investors post more collateral. Miss the deadline and the system force-sells your holdings automatically. This chain reaction is what pushed the VN-Index down 100 points in the first quarter-hour of trading.

SSI Securities Chairman Nguyen Duy Hung posted on Facebook: "Does the Vietnamese stock market really need to panic this badly over oil prices rising because of the Iran conflict?"

His view: many stocks had already been pushed to unreasonably low valuations.

Two Scenarios From Here

VNDirect Securities outlined two paths in early March.

If the conflict cools within weeks and stays short of a full regional war, market sentiment should gradually recover. Investors would refocus on domestic fundamentals — shareholder meeting season, corporate plans for 2026, Q1 macro data, and FTSE Russell's March review of Vietnam's market upgrade. Under this scenario, VNDirect sees the VN-Index retesting 1,900 by late Q1 or early Q2.

If the conflict escalates into a full-scale regional war and oil stays above USD 100 for an extended stretch, the damage runs deeper — global growth takes a hit, inflation reignites, and Vietnam's stock market faces sustained pressure.

VNDirect also pointed out that sell-offs driven by geopolitical events are usually short-lived. They rarely become prolonged bear markets.

The FTSE Upgrade Still Looms

There's a structural catalyst sitting in the background: FTSE Russell is expected to conduct an interim review of Vietnam's market upgrade in March 2026.

Vietnam was confirmed for reclassification from Frontier to Secondary Emerging market status in September 2025, with the official switch set for September 2026. The March review will check whether global brokers are making progress on direct access to the Vietnamese market.

If it goes smoothly, the upgrade could bring around USD 6 billion in passive fund inflows, according to FTSE. The World Bank estimates about USD 5 billion in near-term flows, potentially reaching USD 25 billion by 2030.

Right now, this long-term tailwind is completely drowned out by geopolitical noise. But if the conflict de-escalates, it could quickly become the spark for a rebound.

What It Means for Investors

Short-term, volatility is extreme and visibility is near zero.

Oil prices hinge on the Middle East, and the Middle East changes daily. The cascading effects of margin calls may not be fully worked through yet.

For longer-term investors, though, this is the kind of moment that creates opportunities — if you can tolerate the uncertainty. The SSI chairman is not the only market participant arguing that quality stocks have been dragged down indiscriminately.

But until the picture clears, managing your leverage is far more important than guessing the bottom.